Fixed vs Floating Mortgage Rate: Which One Should You Choose?

- May 2

- 2 min read

Updated: Jun 23

Fixed vs Floating Mortgage Rate Malaysia is one of the most important decisions homebuyers face when choosing a housing loan.

Understanding the differences can help you manage risk, plan your finances and potentially save money over the long term.

Many buyers simply follow what the bank offers — but choosing the right type can save (or cost) you tens of thousands of ringgit over time.

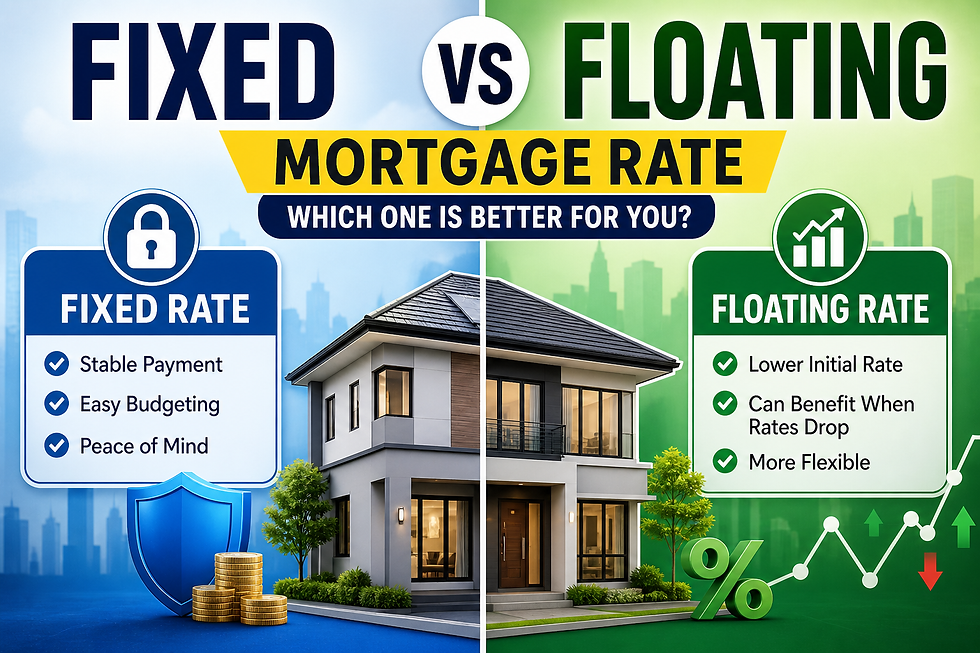

Fixed vs Floating Mortgage Rate Malaysia: Key Differences What Is a Fixed Rate Mortgage?

A fixed rate loan means your interest rate stays the same for a certain period — or sometimes the entire loan tenure.

In Malaysia, fully fixed-rate housing loans are relatively uncommon. Most residential home loans offered by banks are floating-rate facilities linked to the Standardised Base Rate (SBR).

Example:

Loan: RM450,000

Fixed rate: 4.5%

Monthly instalment: stays the same

Even if interest rates go up, your payment does not change

Pros of Fixed Rate

Stable monthly instalment

Easier budgeting

Protection from rising interest rates

Cons of Fixed Rate

Usually higher than floating rates

Less flexibility (early settlement penalties can apply)

You don’t benefit if interest rates drop

What Is a Floating Rate Mortgage?

A floating rate loan (also called variable rate) changes based on the market.

In Malaysia, it is typically tied to:

Bank Negara Malaysia’s Overnight Policy Rate (OPR) = Standardised Base Rate (SBR)

Example:

Rate: SBR + 1.50%

If OPR increases → your instalment increases

If OPR decreases → your instalment decreases

Pros of Floating Rate

Usually lower starting rate

Benefit when interest rates drop

More common and flexible

Cons of Floating Rate

Monthly instalment can increase anytime

Harder to plan long-term

Risk during rising interest cycles

Real Scenario in Malaysia

Let’s say:

Loan: RM450,000

Tenure: 30 years

Scenario 1: Floating Rate (4.3%)

Monthly: ~RM2,227

If OPR increases:

Rate becomes 4.8%

Monthly may increase to ~RM2,361

Scenario 2: Fixed Rate (4.8%)

Monthly: ~RM2,361

Always stays the same

The difference?

Floating starts cheaper — but carries uncertainty.

So… Which One Is Better?

There is no one-size-fits-all answer.

It depends on your situation.

Choose Fixed Rate if you:

Prefer stability and peace of mind

Have tight cash flow

Expect interest rates to rise

Want predictable long-term planning

Choose Floating Rate if you:

Can handle some fluctuation

Want lower initial cost

Expect interest rates to drop

Have strong financial buffer

Most Malaysians choose floating rates — but underestimate the risk.

A small 0.5% increase can significantly affect your cash flow

The real question is:

“Can I still afford my house if my instalment increases by RM200–RM400?”

If the answer is no → fixed rate (or safer loan sizing) may be better.

Common Mistakes to Avoid

Choosing lowest rate without understanding risk

Ignoring future interest rate cycles

Stretching loan to maximum approval

Not having emergency savings

Final Thought

Choosing a mortgage is not just about interest rates.

It’s about:

“How much uncertainty can I handle?”

A slightly higher but stable payment is sometimes better than a cheaper loan that keeps you stressed.

Comments